Nation Outpaces State Economy in Q3, UMass Journal Reports

Declining workforce & interest-rate exposure in key industries make the Commonwealth vulnerable to an economic downturn

October 2022

» Download the detailed report

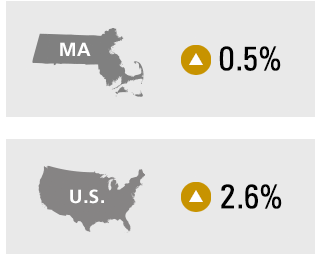

In the third quarter of 2022, Massachusetts real gross domestic product (GDP) increased at a 0.5 percent annualized rate, according to MassBenchmarks, while U.S. GDP increased at a 2.6 percent annualized rate according to the U.S. Bureau of Economic Analysis (BEA). In the second quarter of this year, the BEA estimates that Massachusetts GDP decreased at an annual rate of 2.6 percent while the U.S. declined at a just revised 0.6 percent rate. In the first quarter of this year, the BEA’s annualized growth estimates showed declines of 0.9 percent for Massachusetts and 1.6 percent for the U.S. The Commonwealth’s growth has lagged that of the U.S. in three of the last four quarters.

In the third quarter of 2022, Massachusetts real gross domestic product (GDP) increased at a 0.5 percent annualized rate, according to MassBenchmarks, while U.S. GDP increased at a 2.6 percent annualized rate according to the U.S. Bureau of Economic Analysis (BEA). In the second quarter of this year, the BEA estimates that Massachusetts GDP decreased at an annual rate of 2.6 percent while the U.S. declined at a just revised 0.6 percent rate. In the first quarter of this year, the BEA’s annualized growth estimates showed declines of 0.9 percent for Massachusetts and 1.6 percent for the U.S. The Commonwealth’s growth has lagged that of the U.S. in three of the last four quarters.

Despite the apparent improvement in output growth in the third quarter, the Massachusetts economy appeared to slow along other dimensions, as job growth decelerated, the labor force shrunk (in absolute terms and as a share of the population), and weaknesses emerged in the sectors most affected by rising interest rates, most notably housing. Inflation does not appear to be accelerating but remains well above the target levels set by the Fed. Consumer spending has remained robust, but as inflation continues to undermine household wage gains and erode the savings stockpiles accumulated during the pandemic, spending is likely to slow going forward. The Massachusetts economy may be more vulnerable than that of the U.S. for reasons discussed below.

Payroll employment growth in both the state and the nation decelerated over the last year. Compared to the third quarter of last year, there were 3.8 percent more jobs in Massachusetts in the third quarter of 2022. However, job growth in the second quarter slowed to a 3.7 percent annual rate and eased further in the third quarter (2.2 percent). The U.S. followed a similar pattern with 4.0 percent job growth year over year, 3.3 percent in the second quarter, and 3.1 percent in the third quarter. This deceleration may be related to the shrinking pool of available workers as the recovery from the COVID downturn has progressed to its later stages. In September, the unemployment rate in Massachusetts stood at 3.4 percent, down from 5.1 percent in September 2021. More recently, the declining unemployment rate has been in part the result of a declining workforce — in September 2022 the labor force was smaller than in September 2021 — underscoring the challenge presented by a scarcity of available workers going forward. The U.S. unemployment rate stood at 3.5 percent in September, down from 4.7 percent in September 2021. In September, the number of payroll jobs nationally exceeded the pre-COVID peak of February 2020 by 0.3 percent. Massachusetts remains 1.3 percent below the February 2020 peak.

Inflation, consumer spending, and interest rates have affected sectors of the economy differently. Rising mortgage rates have dramatically slowed transactions in the housing market and consumer spending on household goods like furniture and appliances that are associated with home buying and new household formation.

At the same time, consumer spending on services such as travel, leisure, and hospitality has increased robustly. Through August, real U.S. consumer spending was still rising, with increases in services more than offsetting declines in real goods spending. In Massachusetts, nominal spending on goods subject to the state sales tax and motor vehicle tax fell in the third quarter at a 5.1 percent annual rate, but this followed very sharp growth in the second quarter. Relative to the third quarter of 2021, such spending in Massachusetts was up 7.8 percent in the third quarter of 2022, outstripping inflation.

“Technology, banking, and finance have been hurt by rising interest rates and asset value declines,” noted Alan Clayton-Matthews, Senior Contributing Editor and Professor Emeritus of Economics and Public Policy at Northeastern University, who compiles and analyzes the Current and Leading Indexes for MassBenchmarks.

“With a concentration in information technology and biotechnology, Massachusetts is especially vulnerable to the effects of higher interest rates on the supply of venture capital and private investment. Several tech companies have announced hiring slowdowns, pauses, or layoffs and the tech-heavy NASDAQ and Massachusetts Bloomberg stock indexes have both performed significantly worse than the S&P 500 and the Dow Jones indexes,” Clayton-Matthews added.

Massachusetts wage and salary income growth has lagged that of the U.S. and has fallen far short of inflation on a per-worker basis. The U.S. Bureau of Economic Analysis reported annualized nominal wage and salary income growth in Massachusetts in the second quarter of only 3.9 percent, relative to U.S. wage and salary growth of 6.9 percent. This trend appears to have continued in the third quarter. Based on state withholding taxes, MassBenchmarks estimates that Massachusetts wage and salary income grew at a 3.3 percent annualized rate in the third quarter, as compared to 7.9 percent for the for U.S. (BEA’s estimate of U.S. wage and salary growth in the third quarter will be released Friday, along with revisions to the second quarter estimates.) On an average per-payroll-worker basis, Massachusetts nominal wage and salary income grew at a meager 0.2 percent rate in the second quarter and 1.1 percent in the third quarter. The Boston CPI-U price index in the third quarter increased 7.6 percent from the third quarter of 2021 for all items and 4.9 percent excluding food and energy. The corresponding all metro areas CPI-U inflation rate for the U.S. was 8.3 percent for all items and 6.3 percent excluding food and energy.

The outlook for the rest of this year and for the first quarter of 2023 calls for slower growth, with a real possibility of outright declines in output. Economists who contributed to the Wall Street Journal’s October survey of forecasters on average projected U.S. real annualized GDP growth of 0.4 percent in the fourth quarter and a decline of 0.2 percent in the first quarter of 2023, and assigned a 63 percent probability of a recession by October 2023. The MassBenchmarks leading index is projecting annualized rates of decline in state GDP of 0.5 percent in the fourth quarter and 1.2 percent in the first quarter of next year, respectively.

While these projections are speculative and based on a limited set of leading economic indicators, given the Commonwealth’s older demographic profile (holding back labor force growth) and its exposure in the interest-sensitive technology sector, the risks to the state’s economic outlook are decidedly skewed to the downside.